Tanzania has a unique opportunity to become a major exporter of food crops, especially maize and rice, to the eastern Africa region. It has fertile and abundant crop land to expand production, a transport advantage over countries to the south, and the region has growing import demand. This export opportunity has been hampered in the past by the periodic use of export bans to address food security concerns. However, new research done under the SERA Project of the USAID Feed the Future Initiative has shown that the export bans are not effective at ensuring food security, controlling food prices, or preventing exports. It is now time to re-think the food crops export ban as a way of dealing with food security concerns and to focus on expanding exports to raise incomes of farmers. New programs will also be needed to deal with food security.

Peri-urban growth in Zambia faces particular challenges due to the interface of state and customary land administration systems with different stakeholders using land under leasehold and customary tenure regimes. The lack of structures to document these landholdings, share information, or resolve disputes between state and customary institutions presents risks to realizing sustainable development in peri-urban areas. This brief presents recent illustrations based on news media accounts of customary and state institutional overlap, planning and service delivery gaps, conversion of customary to leasehold land tenure, risks to public lands, and an inadequate land information system each of which contributes to peri-urban tenure insecurity. It concludes by identifying opportunities for protecting the rights of peri-urban customary smallholders and new urban settlers, promoting economic growth, reducing conflict, and improving resource management through the following four areas of work and twelve actions/recommendations, many of which are already conceptualized by the Government of the Republic of Zambia, but require additional support to be realized. These recommendations include:

Establish the current status of peri-urban land by: 1) developing an empirical understanding of peri-urban land tenure dynamics through targeted research; and, 2) documenting and making accessible state and customary land tenure information.

Recognize and protect existing rights by: 1) strengthening the recognition of the rights of existing peri-urban smallholders and residents of informal settlement; 2) protecting remaining public lands in peri-urban areas; and, 3) upgrading and planning informal settlements.

Respect and build on the technical capacities of government and the local legitimacy of customary institutions to improve rural/urban land governance by: 1) clarifying the role of chiefs in customary land under statutory tenure; 2) developing improved guidelines for consultation and consent around land conversion; 3) creating communication channels among councils and traditional leaders on land management; and, 4) developing and training local land tribunals composed of government and customary authorities.

Develop a Land Policy and associated legislation that integrate land administration and land useplanning by: 1) ensuring the Land Policy addresses the issue of land rights in peri-urban areas; 2) designing legislation that can address challenges at the urban/rural interface; and, 3) bringing peri-urban and rural areas into the national planning process, while respecting the roles of all stakeholders and legitimate leaders.

Increasing farmers’ awareness on types of contracts used in the management of agricultural lands

Photo by: USAID/Feed the Future Tajikistan Land Market Development Activity

Contracts are crucial to success in the agricultural sector. Ms. Safarova Shahbonu, head of dehkan farm Zuhal, noted that “the harvest was very low this year as the seeds and mineral fertilizers were not of good quality. Since I did not have a signed contract with the supplier of seeds and fertilizers, but rather a verbal agreement, I could not stake a claim and protect my rights.”

Since farmers do not know what types of agriculture-specific contracts exist or how to formally sign them, they can face misunderstandings in most cases, and at worst deceit. Through grantee training organizations, the Feed the Future Tajikistan Land Market Development Activity informs farmers on the benefits of written contracts, as well as provides resources to support their use.

Mr. Burgut Abdulvohidov, tashabbuskor from the Vahdat jamoat of Vakhsh district, was aware of this issue and invited LMDA grantee public organization Mahbuba to organize a training on types of contracts used in the agricultural sector. Twenty five farmers from the jamoat participated in the training, which provided information on the types of contracts available for agricultural deals. After the training, the farmers realized the importance of signing written contracts and were empowered to utilize them.

Ms. Shahbonu Safarova, head of dehkan farm Zuhal, was one of the first training participants to execute a written contract, with support from a legal aid center lawyer. The contract outlines the rights and responsibilities of both parties, preventing any possible misunderstandings and protecting her interests.

“Having participated in the training, I understand the importance of written contracts in the agricultural sector. From now on, I will carry out all my agricultural activities by signing a written contract, thus preventing a violation of my rights.” — Ms. Shahbonu Safarova, head of dehkan farm Zuhal

After taking part in these trainings, farmers are now aware of how to execute contracts for any agricultural activity in which they are interested. Moreover, the Feed the Future Tajikistan Land Market Development Activity printed and distributed a brochure containing information on the types of contracts used in the management of agricultural lands, complete with contract templates. By providing access to information and templates, as well as the advantages and disadvantages of each type of contract, the Feed the Future Tajikistan Land Market Development Activity empowers land users to execute formal written contracts and protect their land use rights.

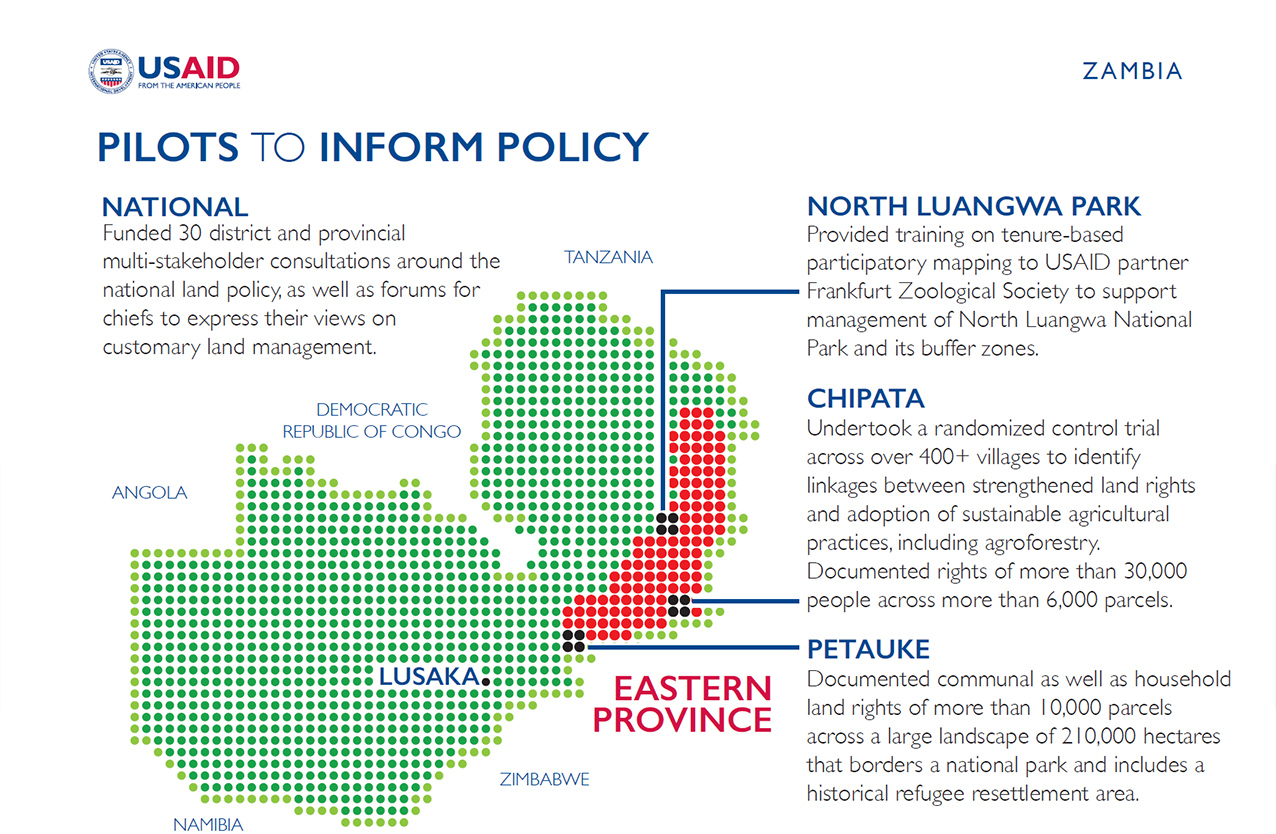

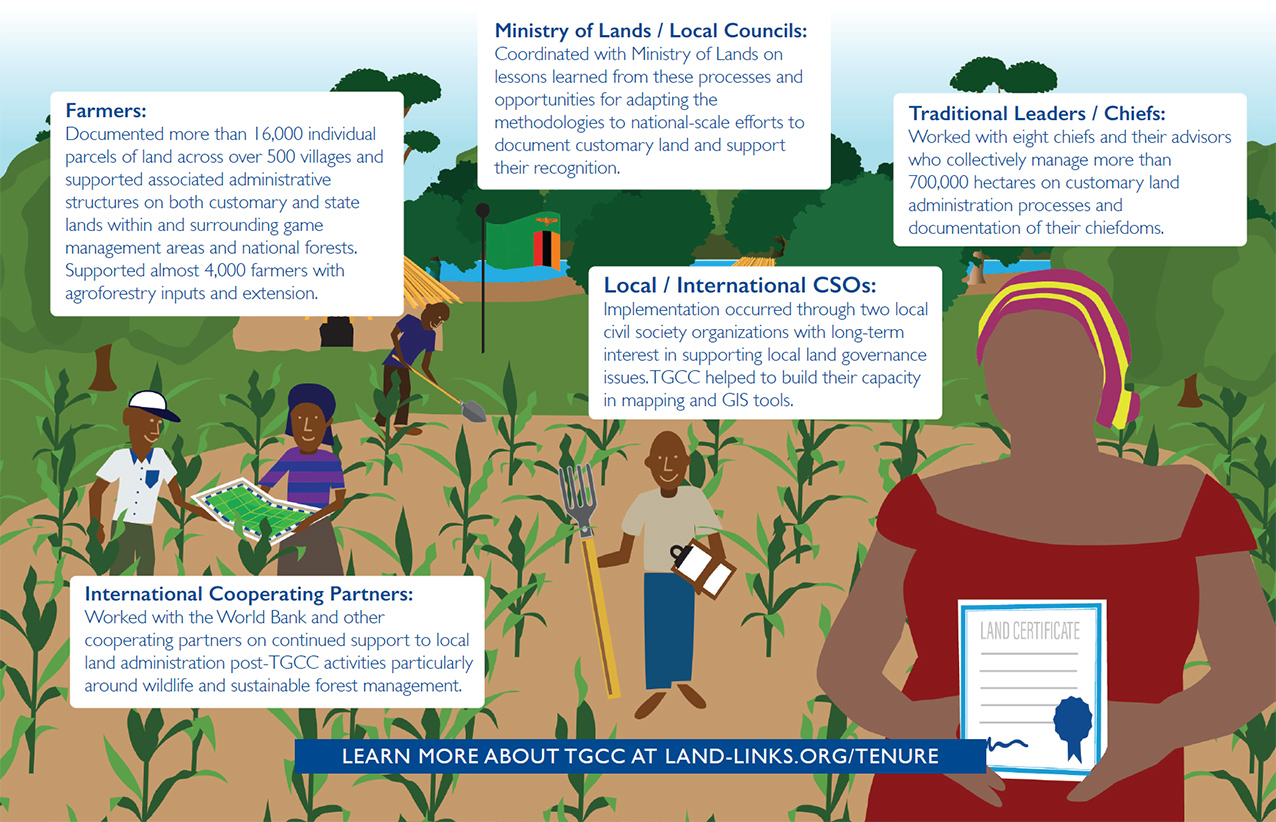

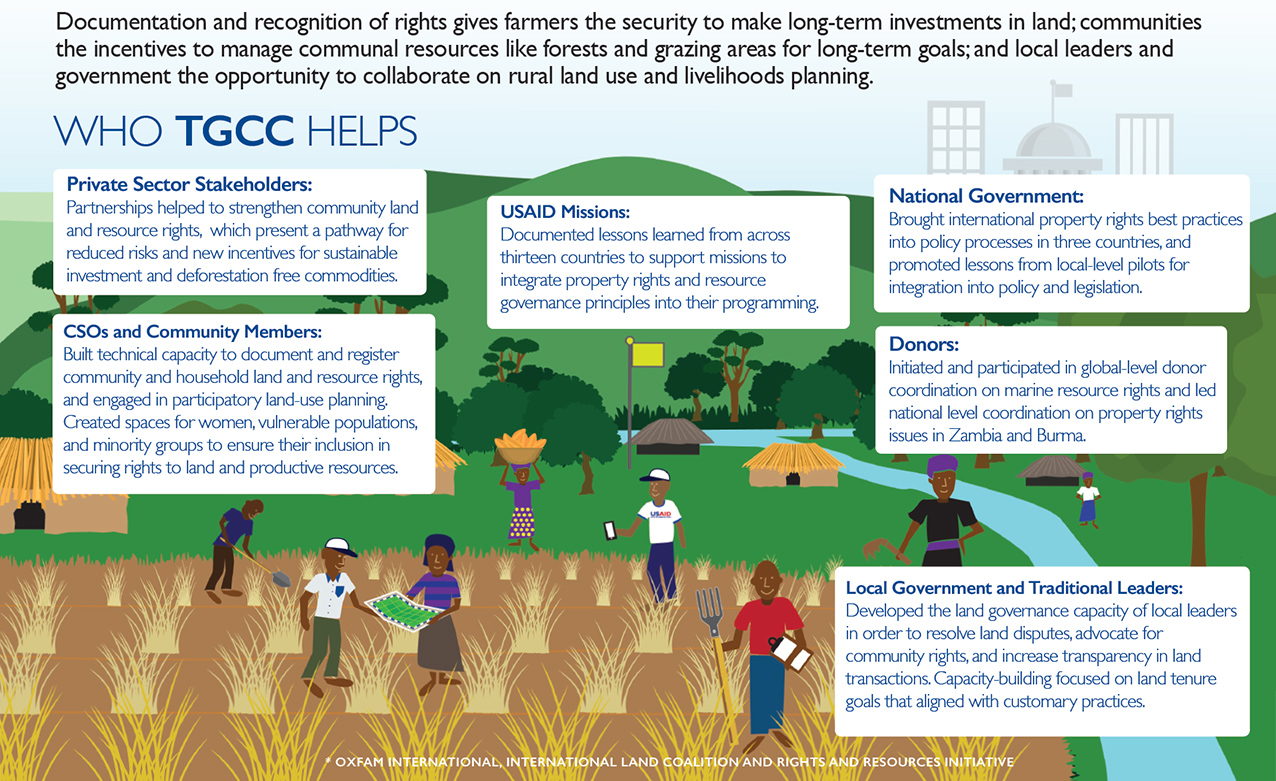

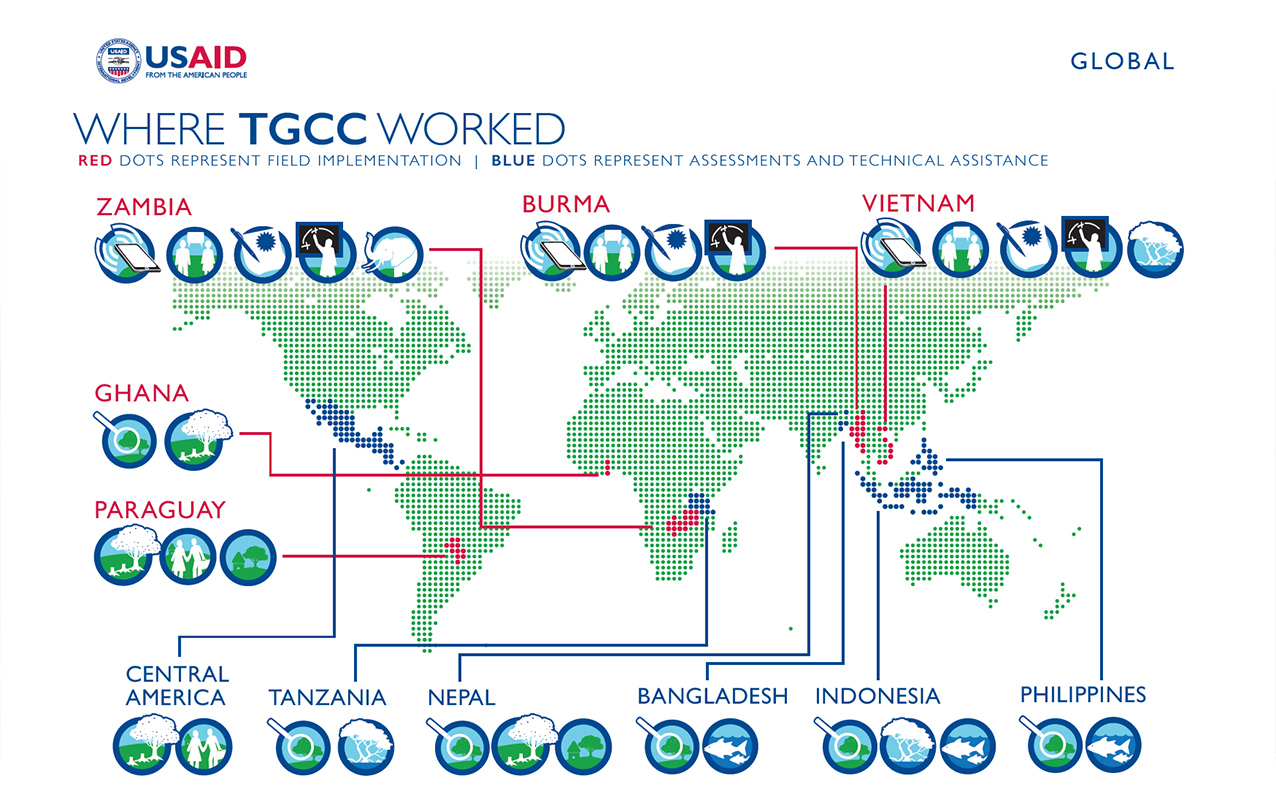

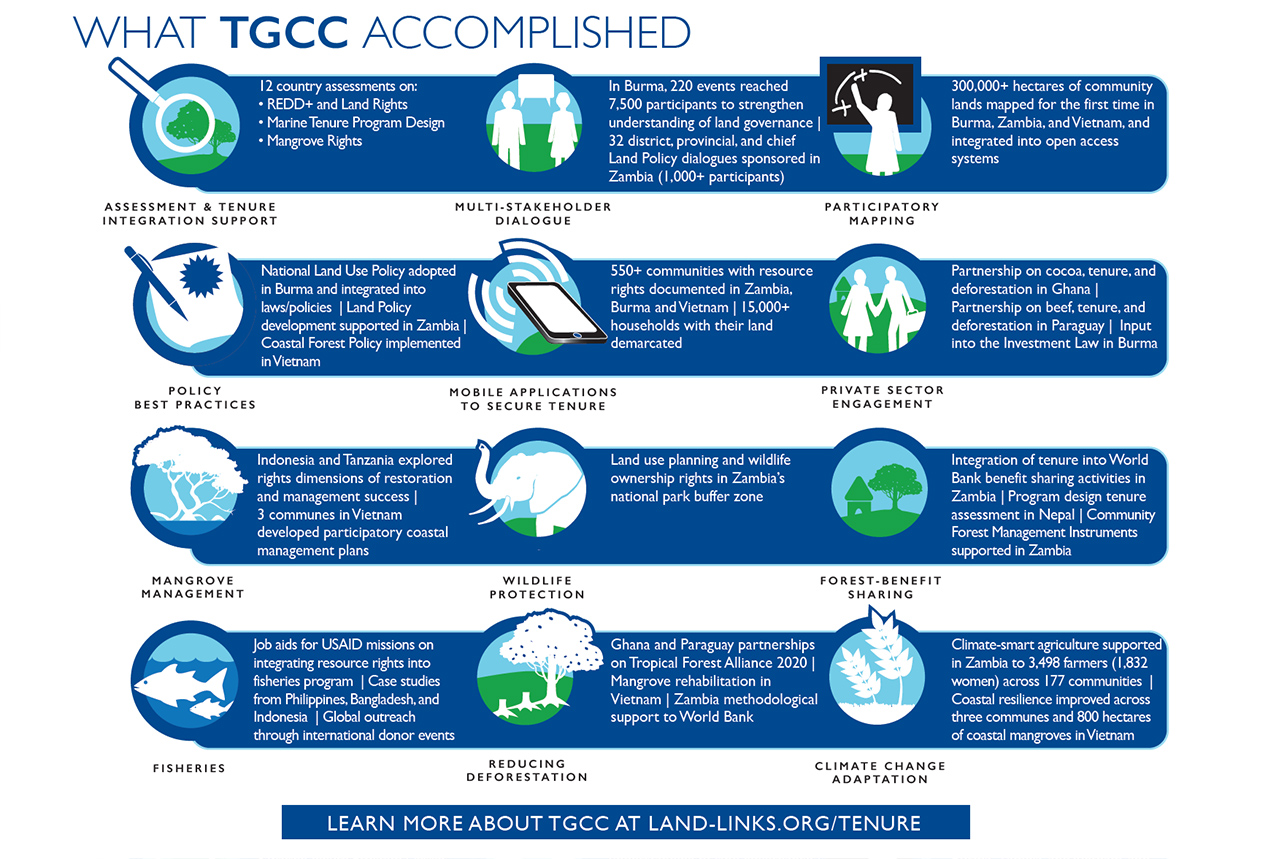

National governments increasingly recognize the importance of legal recognition and documentation of customary rights. With hundreds of millions of unregistered land claims globally, rapid and robust approaches are needed to document and administer communal and household rights in the long-term. USAID’s Tenure and Global Climate Change (TGCC) Program piloted customary land documentation processes in Zambia that relied on local knowledge and the use of low cost mobile applications to secure tenure (MAST).

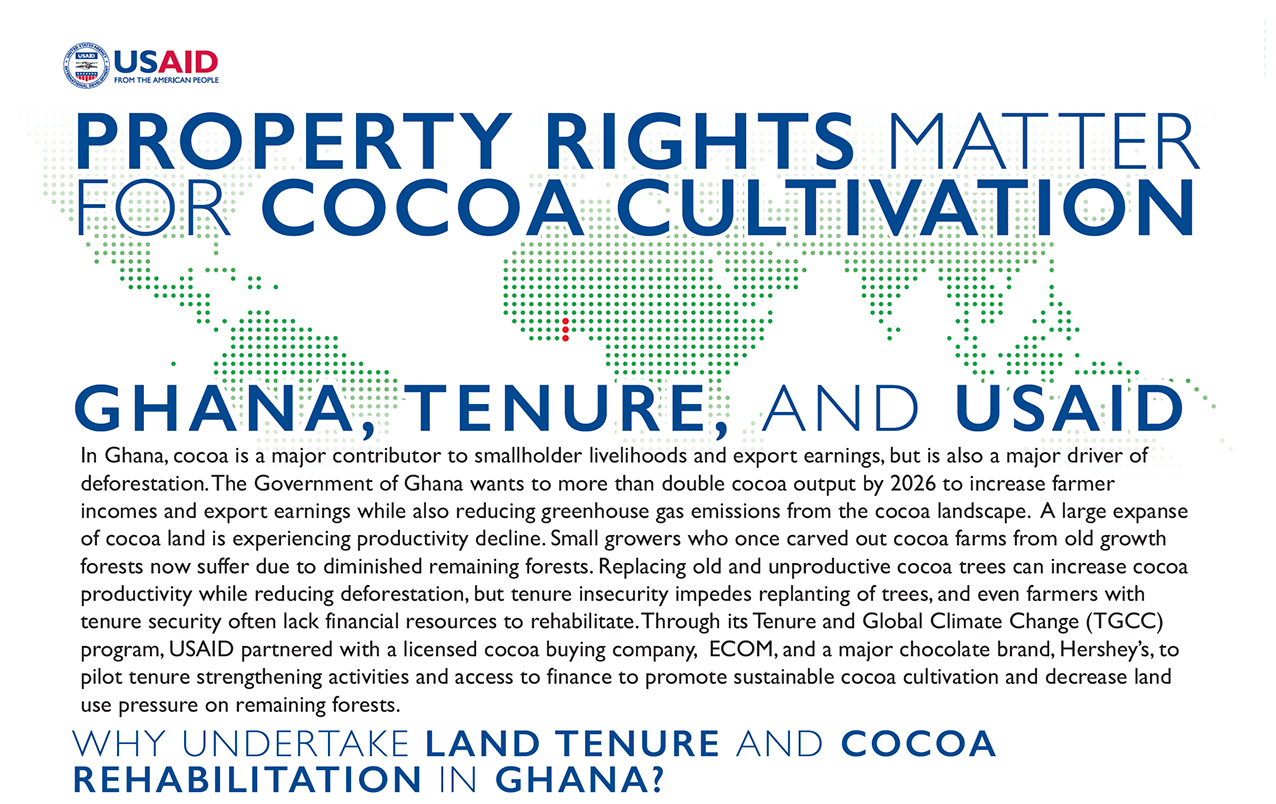

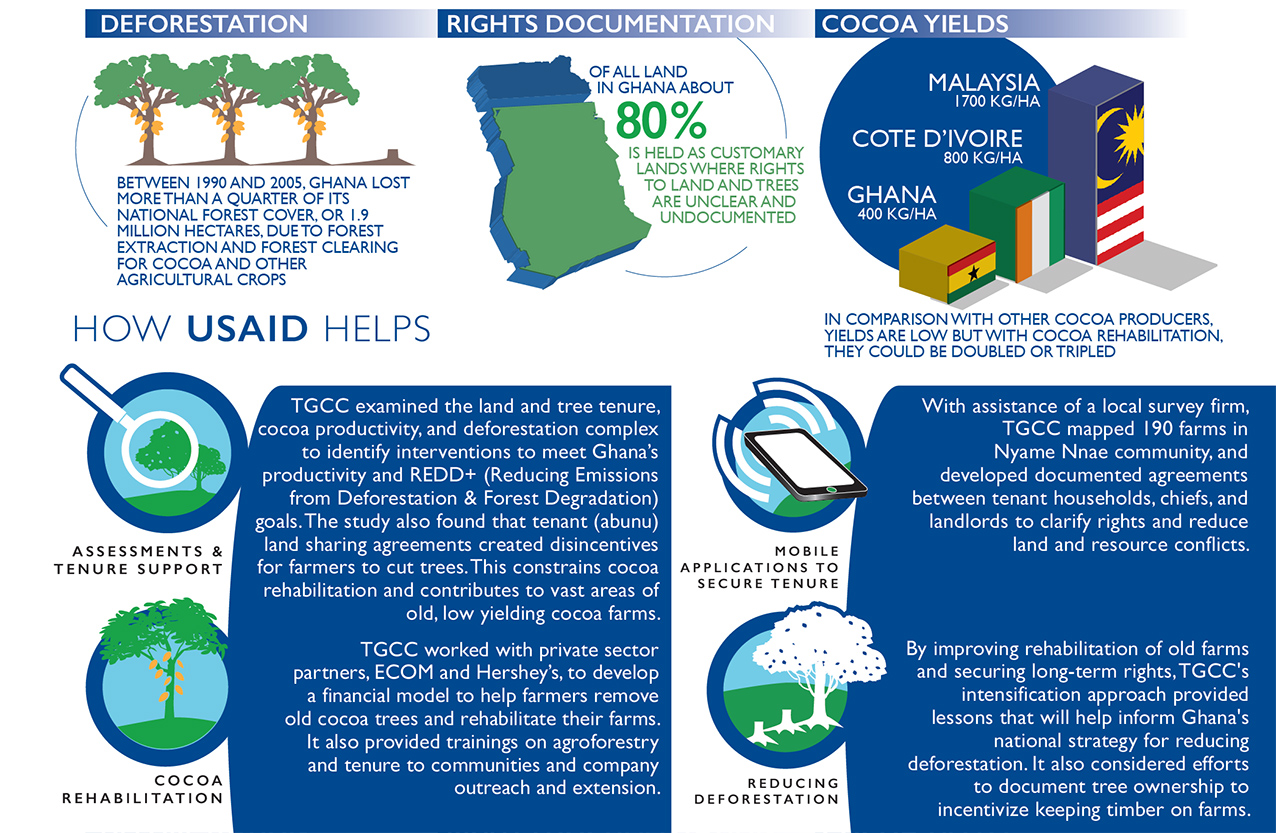

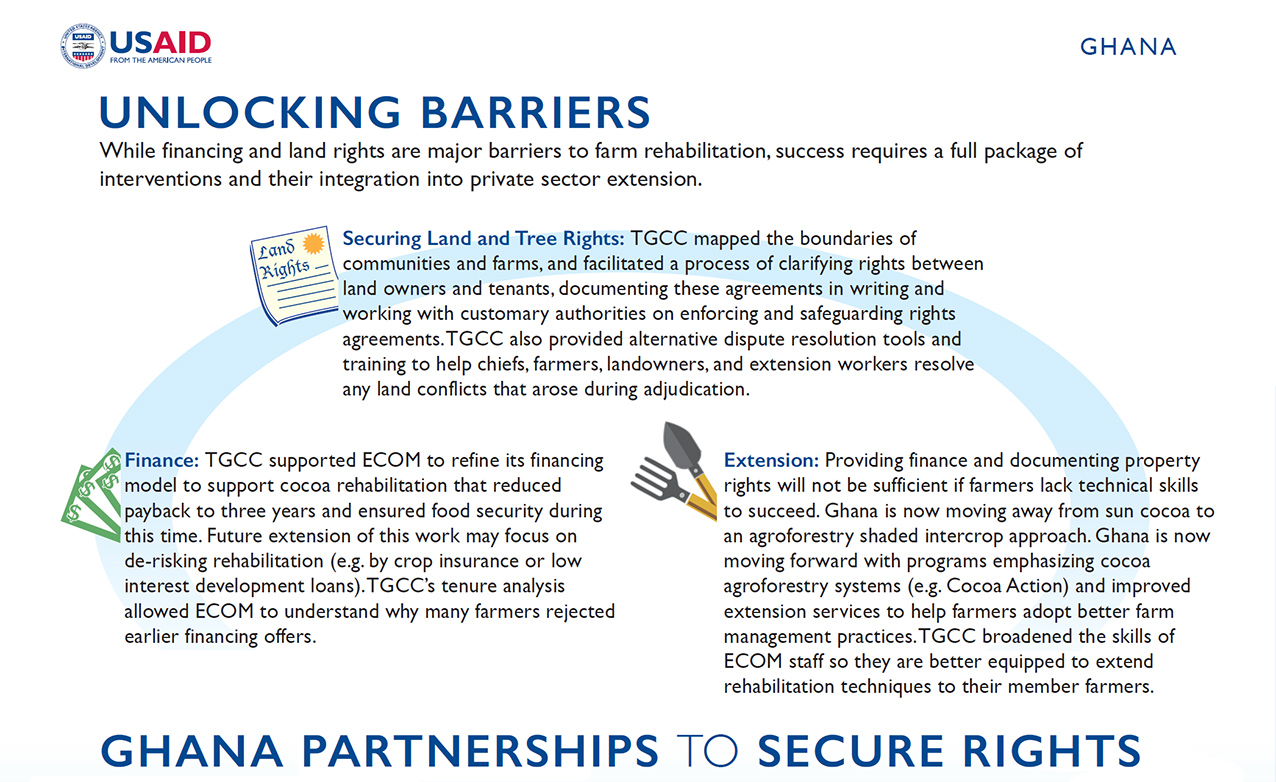

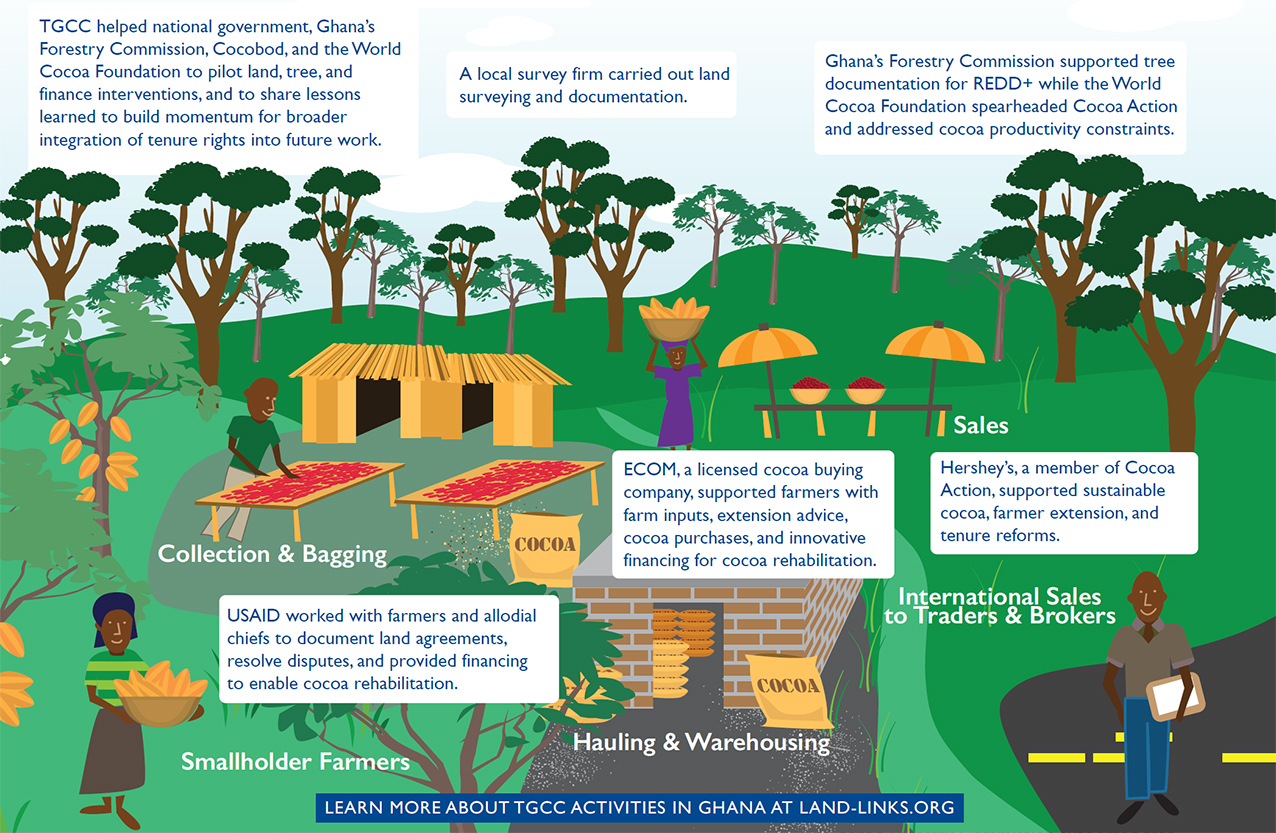

In Ghana, cocoa is a major contributor to smallholder livelihoods and export earnings, but is also a major driver of deforestation. The Government of Ghana wants to more than double cocoa output by 2026 to increase farmer incomes and export earnings while also reducing greenhouse gas emissions from the cocoa landscape. A large expanse of cocoa land is experiencing productivity decline. Small growers who once carved out cocoa farms from old growth forests now suffer due to diminished remaining forests. Replacing old and unproductive cocoa trees can increase cocoa productivity while reducing deforestation, but tenure insecurity impedes replanting of trees, and even farmers with tenure security often lack financial resources to rehabilitate. Through its Tenure and Global Climate Change (TGCC) program, USAID partnered with a licensed cocoa buying company, ECOM, and a major chocolate brand, Hershey’s, to pilot tenure strengthening activities and access to finance to promote sustainable cocoa cultivation and decrease land use pressure on remaining forests.

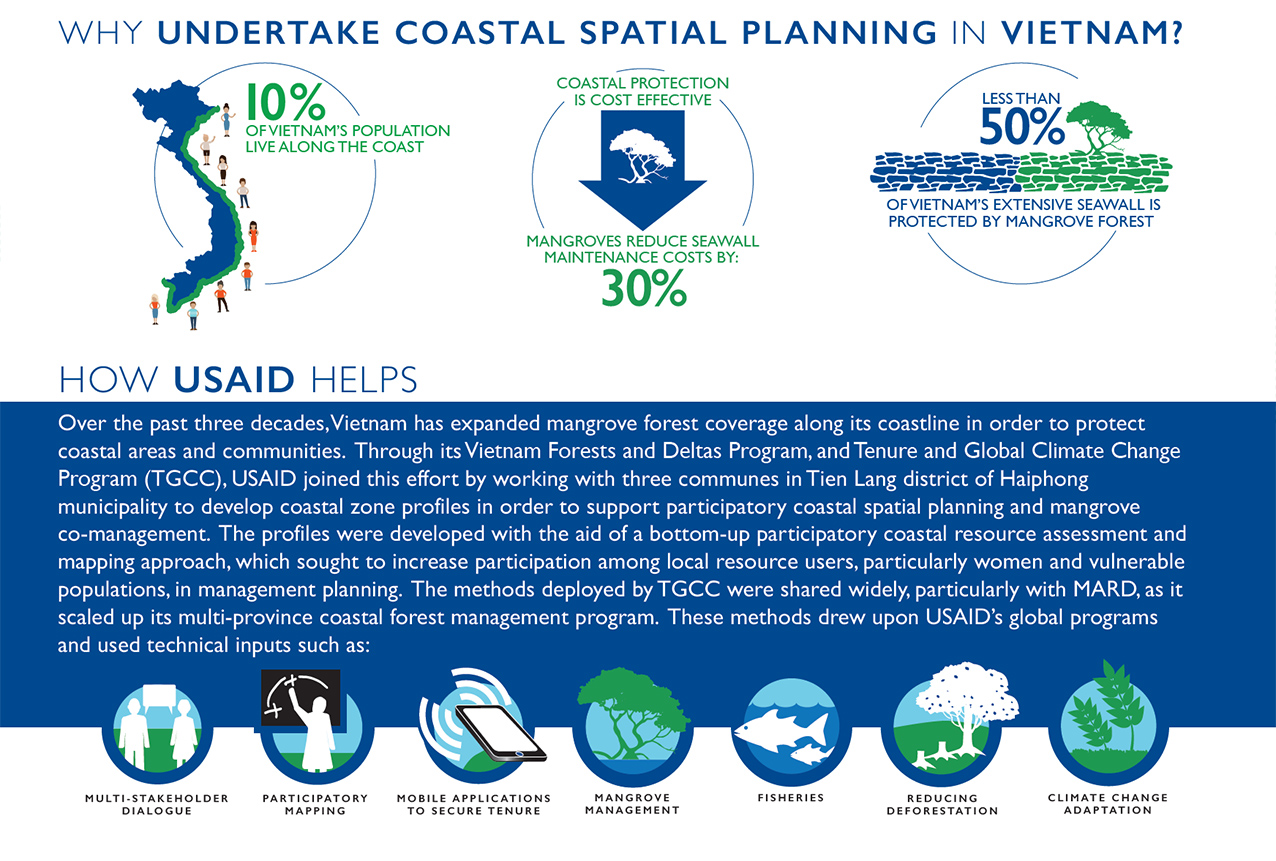

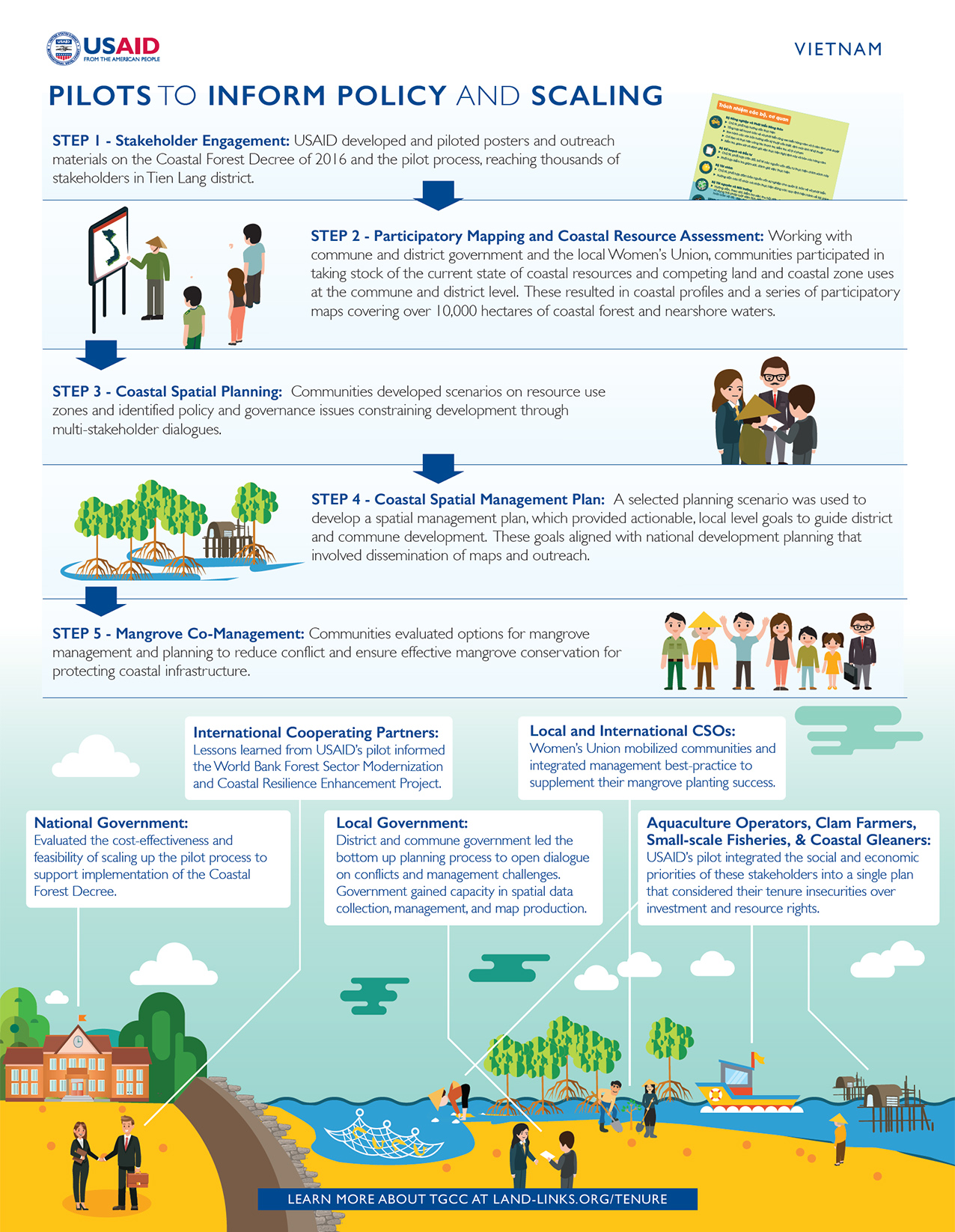

Vietnam looks to the sea for livelihoods and economic growth. With 9 million people living in coastal areas, many of which rely on the protection of seawall systems and mangrove forest, Vietnam has a high degree of vulnerability to coastal erosion, storm surge, and sea level rise. In this coastal landscape, there is a complex mix of uses from gleaning a variety of aquatic resources, to small-scale fisheries, to aquaculture, and clam farming. At times, there can be conflicts between these differing uses. The Government of Vietnam has a number of policies and laws related to coastal zone management that address this important resource and, in 2016, added a Coastal Forest Decree to improve the consistency of coastal forest management, including mangrove forests. In support of this decree, USAID, partnering with the Ministry of Agriculture and Rural Development (MARD), piloted participatory coastal spatial planning and mangrove co-management processes to inform coastal zone management, as well as to support vulnerable livelihoods in the face of economic and environmental changes.

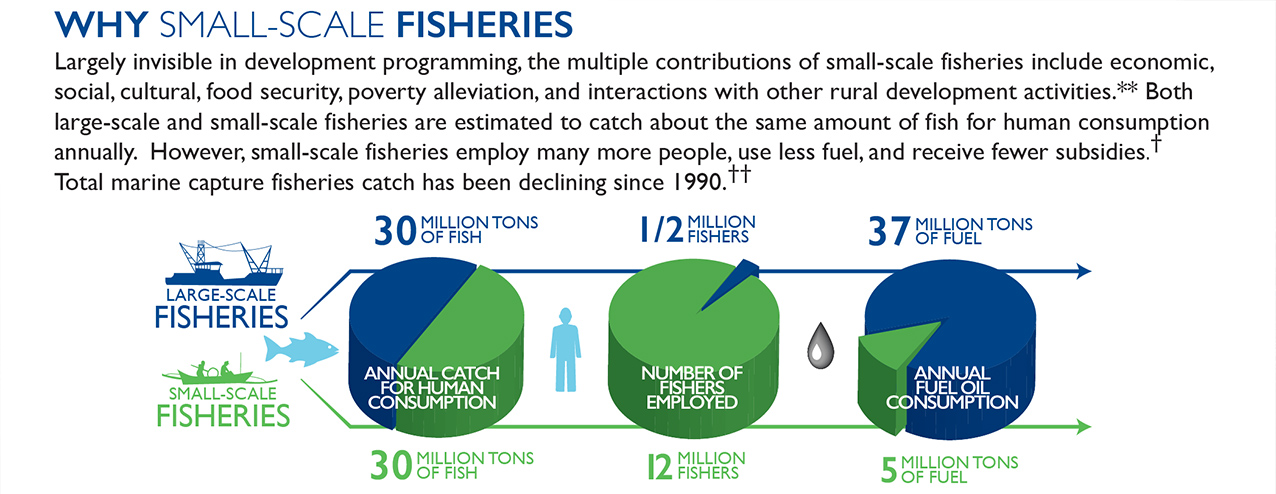

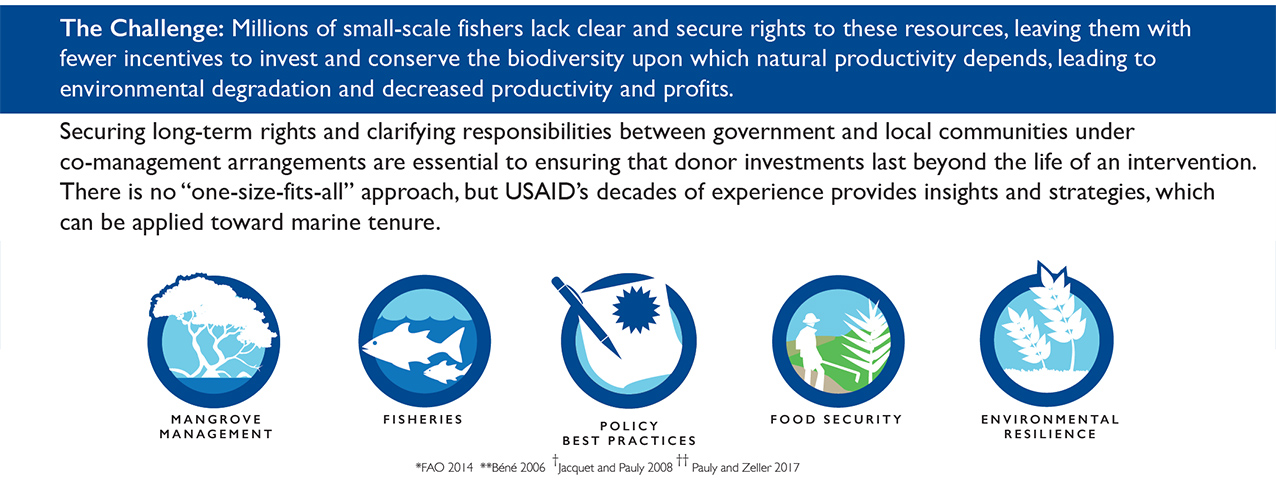

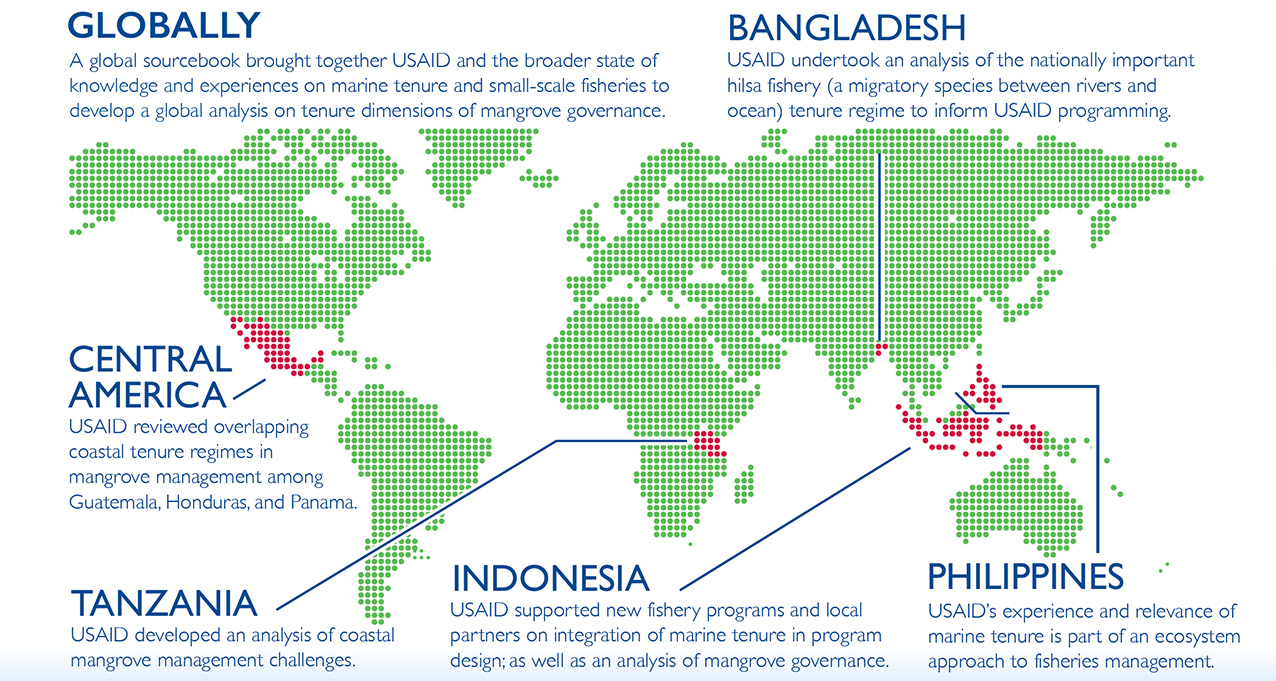

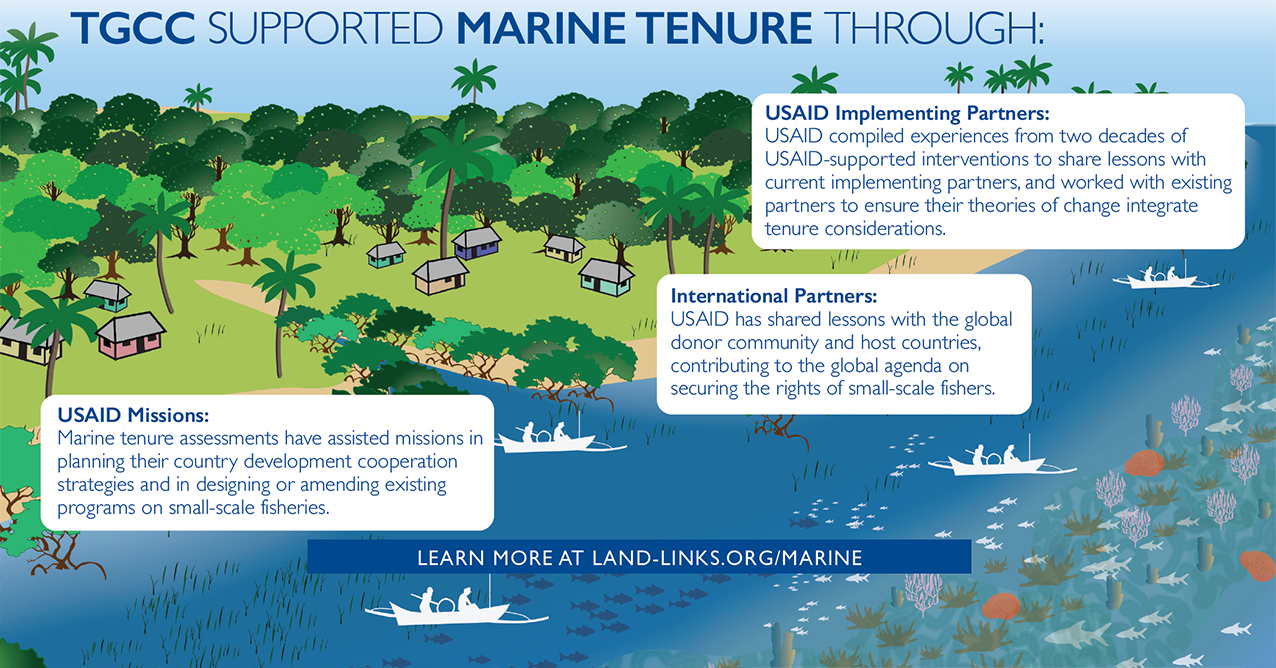

Fish remains among the most traded food commodities worldwide, worth almost US$130 billion in 2012.* Marine tenure is the set of rights and responsibilities in coastal and marine environments that define who is allowed to use resources, in what way, for how long, under what conditions, and how those rights can be transferred. Formal recognition of marine tenure provides communities with the necessary security to invest in and manage their fishery resources for the long-term.

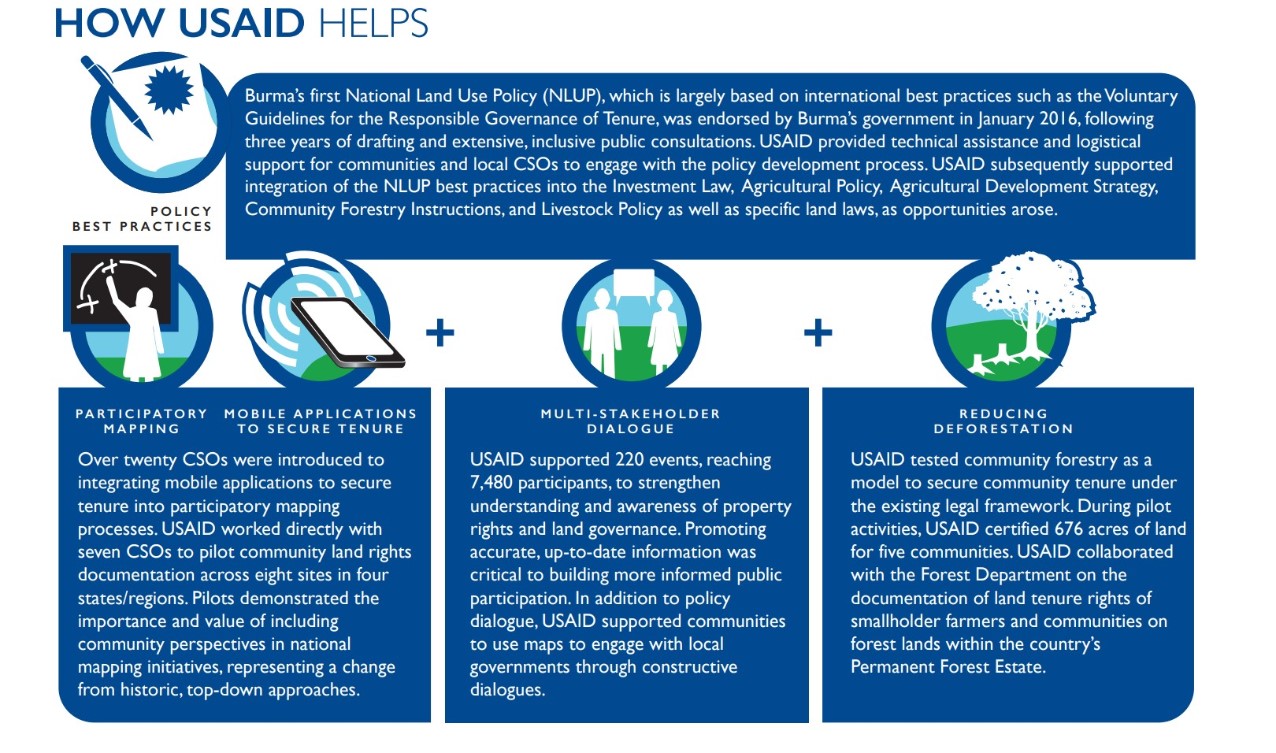

Burma is undergoing a period of historical transition with the electoral victory of the National League for Democracy in 2016 representing a change after fifty years of military rule. Burma has a profusion of antiquated and poorly harmonized laws related to land and forest rights, as well as a widespread lack of legal documentation and awareness of those rights by its rural citizens who represent 70% of the population. At the same time, the country’s recent economic opening has led to concerns that extractive and agribusiness investments may undermine the land tenure and property rights of this rural population.

USAID recognizes the critical role of land in building a robust and inclusive economy, promoting democracy, and improving the livelihoods and well-being of Burma’s people. As a result, USAID’s Tenure and Global Climate Change (TGCC) Program is supporting inclusive land policy and legislation development in Burma, as well as piloting of participatory mapping processes using low cost mobile applications to secure tenure (MAST). TGCC increases dialogue between local government, communities and land-related stakeholders.

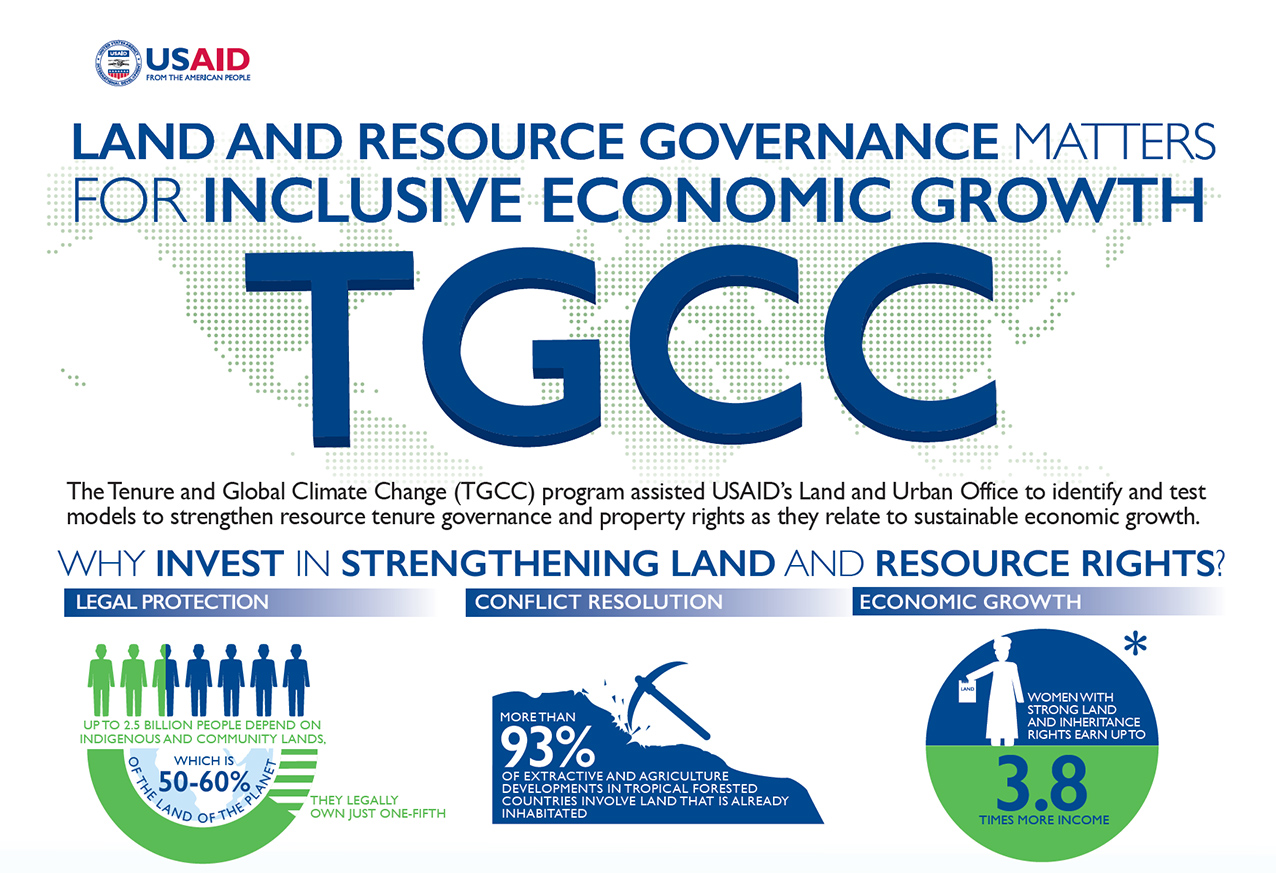

The Tenure and Global Climate Change (TGCC) program assisted USAID’s Land and Urban Office to identify and test models to strengthen resource tenure governance and property rights as they relate to sustainable economic growth.

U Win Thein, Chief Minister for Bago Region, offers opening remarks at the Lessons Learned Workshop on Land Use Planning for Bago Region.

At a one-day workshop in Bago, Bago Region, three donor-funded projects introduced findings from pilot activities examining land use planning approaches at regional, township, and village tract levels. Implemented by the European Union at the regional level, OneMap Myanmar at the township level, and the USAID-funded Land Tenure Project (LTP) at the village tract level, the three projects shared their findings with government officials from nine departments to compare different approaches.

Land use planning in Burma is at a very early stage and, historically, has occurred at higher levels of government without taking into account the perspectives of communities. Together, the pilots demonstrated how land use planning can benefit from the integration of both top-down and bottom-up land use planning techniques. For example, land use classifications determined at the regional level using remote sensing techniques need to be integrated with community perspectives on their land uses. Participants indicated that many of the data-driven and forward-looking concepts presented at the workshop were new. In particular, since community voices have not traditionally been taken into consideration in planning matters, the village tract level approach piloted by USAID LTP was considered a good demonstration of the value of community level participation. A regional official noted, “We are now in the democratic era and need to use the bottom-up approach and start implementing it. Then we can have proper and correct decisions for the public.” This engagement marked an initial, but important, step toward integrating land use planning at multiple scales in Burma.

Development of inclusive land use planning approaches is essential for sustainable, long-term economic development of urban and rural communities in Burma. Effective land use planning builds the capacity of government institutions and related stakeholders to implement policy, legal, and regulatory frameworks that strengthen long-term stability and prosperity.